|

Search HansaManuals.com HansaManuals Home >> Standard ERP >> Accounting Principles >> Chart of Accounts Previous Next Entire Chapter in Printable Form Search This text refers to program version 8.0 Objects A properly formulated Chart of Accounts allows you to analyse your company's activities, but the level of this analysis is limited. For example, it may allow you to analyse your sales and cost of sales by type of Item, but you will not also be able to analyse them by geographical area, type of business, salesperson or department.Normally, a typical business will require three basic levels of analysis:

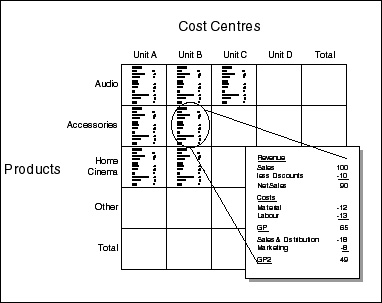

Conceptually, the accounting situation can be illustrated using a three-dimensional table:

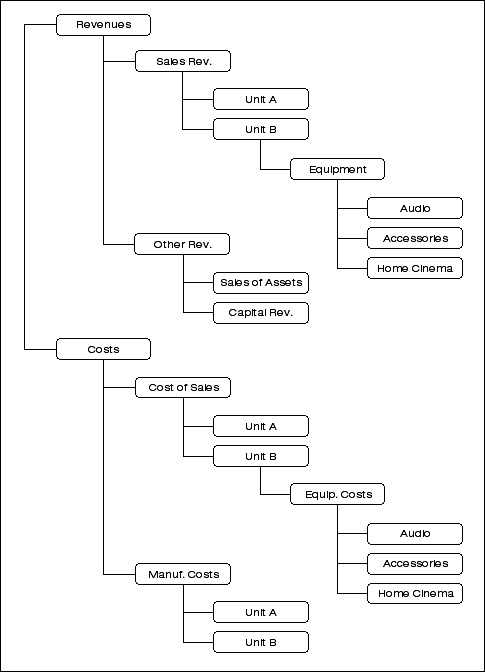

To simplify the structure many accounting systems subdivide the "account string" into different parts, each indicating cost type, department, project, product etc. This is only a partial solution. The only logically viable solution to truly multi-dimensional accounting is to use an "Object" classification in each accounting transaction. Using this method, the Chart of Accounts will contain account specifications for the kind of revenue, expenditure, asset, liability or equity, while the Objects will represent the remaining information (i.e. cost type, department, project, product etc). Each accounting transaction will consist of an Account Number, an amount, a date, and one or more Object classifications. Referring to the illustration above, a wages payment for selling radios in Unit B would contain the following information: Number 970001 This Object classification makes it simple to show every transaction entered for each product, unit and cost type, and to produce separate profit and loss statements for each section of the business (e.g. to show the profitability of Unit B and of Audio Sales). The use of Objects is not limited to Income and Cost Accounts. You can use Objects with all types of Accounts, including Asset, Liability and Equity Accounts. Click here for a description of how you can use Objects in Standard ERP to obtain the information and analysis that you need to improve the efficiency of your business. --- In this chapter:

Go back to:

|