|

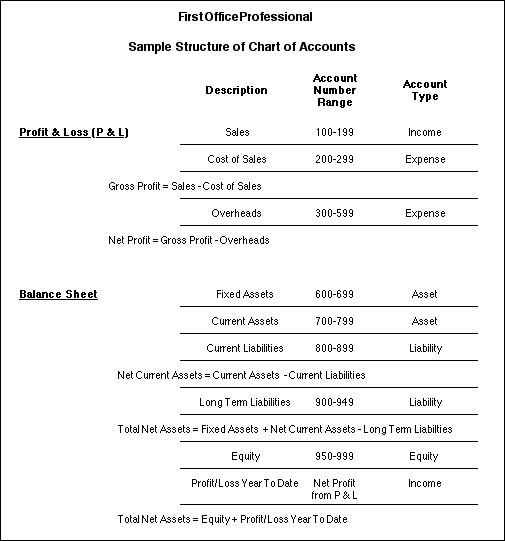

Search HansaManuals.com HansaManuals Home >> Discontinued Products >> HansaWorld FirstOffice Professional >> Accounting Principles >> Chart of Accounts Previous Next Entire Chapter in Printable Form Search This text refers to program version 4.3 Introduction Accounts are the Nominal Ledger headings that you use to classify all financial transactions: each Nominal Ledger Transaction described on these pages posts to two or more Accounts. In fact each Nominal Ledger Transaction can be defined by which Accounts these are. The organisation of these Accounts is known as a 'Chart of Accounts': a systematic list of how assets, liabilities, income and expenses are to be classified and thus the basis for your accounting reports. The logic used in the classification determines the usefulness of your reports, and the drawing up of a satisfactory Chart of Accounts requires careful consideration.In designing a Chart of Accounts, it is usual practice to group Accounts together according to type. For example, all Sales Accounts should have similar codes, different Bank Accounts should have similar codes and so on. This will ensure that they appear together in reports. Room should be left so that new Accounts, the need for which is currently unforeseen, can be inserted in the right place. If your business develops into new products, for example, you should be able to create Sales Accounts for those new products with similar codes to the existing Sales Accounts. In traditional accounting systems, the Chart is divided into account classes, following a decimal classification. Two or three classes are reserved for Balance Sheet Accounts, one class is normally reserved for internal accounting and year-end operations, and the remaining five or six classes are used for revenue and cost classification. Typical Charts of Accounts, including that supplied as a template with FirstOffice, follow the model illustrated below. The Accounts are usually divided into two groups, named after the report in which they appear.

Previous Next Top Entire Chapter in Printable Form |